Contents

Dental Insurance Annual Maximums in 2026: How to Maximize Every Dollar of Your Benefits

Your dental insurance annual maximum is arguably the single most important number in your benefits package, yet it is also the most frequently misunderstood. It determines the absolute ceiling on what your insurer will pay for your dental care in a given year -- and once you hit it, every additional dollar comes out of your own pocket. In 2026, the average annual maximum has barely budged from where it was decades ago, even as the cost of dental care has climbed steadily. Understanding how this cap works, what counts toward it, and how to plan around it can save you hundreds or even thousands of dollars each year.

What Is a Dental Insurance Annual Maximum?

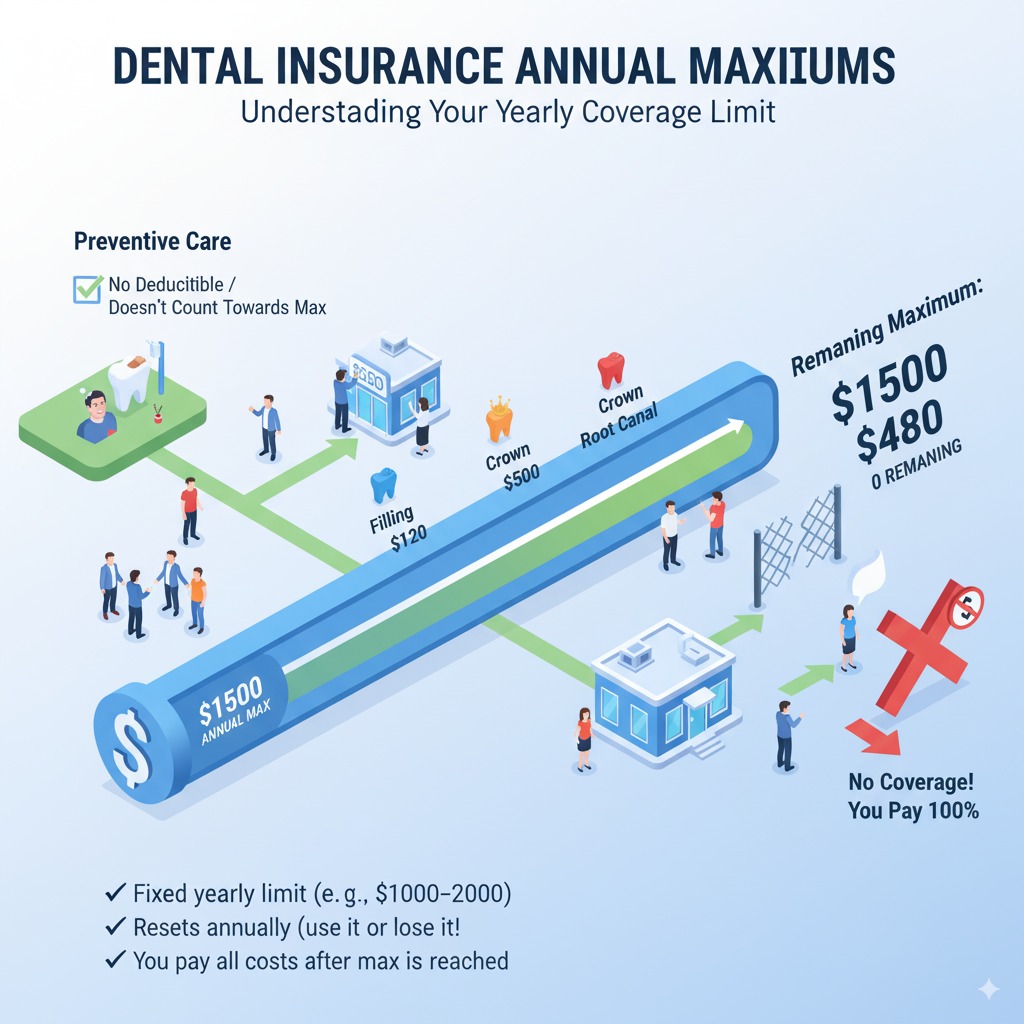

The annual maximum (sometimes called the annual benefit maximum or yearly cap) is the total amount your dental insurance plan will pay toward covered services during a single benefit year. Once the insurer's payments reach this limit, you become responsible for 100% of any remaining costs until the benefit year resets.

For example, if your plan has a $1,500 annual maximum and your insurer has already paid $1,500 toward your cleanings, fillings, and a crown, any additional procedures -- even those normally covered at 50% or 80% -- will be entirely your responsibility until your benefit year rolls over.

Annual Maximums by Plan Type in 2026

Annual maximums vary significantly depending on the type of plan you have and whether it is an individual purchase, an employer-sponsored benefit, or a government program. Here is how the major categories compare in 2026:

| Plan Type | Typical Annual Maximum | Monthly Premium Range | Best For |

|---|---|---|---|

| Basic Individual PPO | $1,000 - $1,500 | $25 - $50 | Healthy adults needing preventive care only |

| Employer-Sponsored PPO | $1,500 - $2,500 | $15 - $40 (employee share) | Employees with moderate dental needs |

| Premium Individual PPO | $2,500 - $5,000 | $50 - $100 | Patients anticipating major work |

| DHMO / Managed Care | No annual maximum (copay-based) | $8 - $25 | Budget-conscious patients near an assigned dentist |

| Dental Discount Plan | No maximum (not insurance) | $10 - $20 | Patients needing extensive work beyond insurance caps |

"The dirty secret of dental insurance is that the average annual maximum of $1,500 has remained essentially unchanged since the 1970s. If it had kept pace with dental inflation, it would be closer to $8,000 today. Patients need to understand that dental insurance is designed to subsidize routine care, not to be a comprehensive safety net for major treatment." -- Dr. Robert Feld, DDS, MBA, Dental Benefits Consultant

What Counts Toward Your Maximum and What Does Not

Understanding what counts against your annual maximum is essential for planning your care:

Counts toward your maximum:

- The insurer's payment for preventive services (exams, cleanings, X-rays)

- The insurer's payment for basic services (fillings, simple extractions, root canals)

- The insurer's payment for major services (crowns, bridges, implants, dentures)

Does NOT count toward your maximum:

- Your monthly or annual premiums

- Your annual deductible payment

- Your coinsurance or copay amounts

- Services not covered by your plan (cosmetic procedures, adult orthodontics on some plans)

The Real Cost of Running Out of Benefits

Exceeding your annual maximum can result in substantial out-of-pocket expenses. Consider this real-world scenario for a patient with a $1,500 annual maximum on a standard PPO plan:

| Service | Total Fee | Insurance Pays | Remaining Maximum | Your Cost |

|---|---|---|---|---|

| 2 Cleanings + Exams | $400 | $400 (100%) | $1,100 | $0 |

| 2 Fillings | $500 | $400 (80%) | $700 | $100 |

| 1 Crown | $1,400 | $700 (50%, capped at remaining max) | $0 | $700 |

| 1 Root Canal (needed later) | $1,100 | $0 (maximum exhausted) | $0 | $1,100 |

| TOTAL | $3,400 | $1,500 | -- | $1,900 |

In this scenario, the patient paid $1,900 out of pocket -- more than what insurance covered. The root canal at the end of the year received zero coverage because the $1,500 maximum had already been exhausted. With strategic planning, this outcome could have been very different.

7 Strategies to Stretch Your Annual Maximum

Smart benefits planning can make a significant difference in how much you pay out of pocket. Here are the most effective strategies for 2026:

Phase Treatment Across Benefit Years

If your dentist recommends multiple crowns or other major procedures, ask about splitting the work across two benefit years. For example, get one crown in November and the second in January. Each procedure draws from a separate annual maximum, effectively doubling your available benefits.

Use Preventive Care Strategically

If your plan does not exempt preventive care from the maximum, schedule your second cleaning early in the year to preserve as much of your maximum as possible for unexpected needs. If your plan does exempt preventive care, take full advantage of it -- these "free" visits often catch problems early when treatment is simpler and less expensive.

Additional strategies include:

- Submit pre-authorization requests before any major procedure to know exactly what your plan will cover and what you will owe.

- Use an FSA or HSA to pay your out-of-pocket costs with pre-tax dollars, effectively saving 25-35% on your share.

- Ask about alternative treatment codes -- some procedures can be coded differently (for example, a core buildup may be coded separately from a crown), which may affect how much counts toward your maximum.

- Coordinate benefits if you have coverage under two plans (your own and a spouse's). The secondary plan can pick up some or all of the patient's share after the primary plan has paid.

- Do not let benefits expire unused. If it is October and you still have $800 remaining in your annual maximum, schedule any overdue treatment before December 31.

"I see patients every year who leave hundreds of dollars of benefits on the table simply because they did not realize their benefit year was about to reset. Unused benefits do not roll over in most plans -- they vanish. Treat your annual maximum like a use-it-or-lose-it account." -- Lisa Morales, RDH, MS, Dental Benefits Coordinator

Plans with Higher or No Annual Maximums

If you know you will need extensive dental work in the coming year, consider these alternatives:

- Premium PPO plans: Some individual and employer plans offer maximums of $3,000-$5,000. Monthly premiums are higher ($60-$100+), but the additional coverage can more than offset the premium increase if you need a crown, implant, or other major service.

- DHMO plans: These plans have no annual maximum because they work on a fixed copay schedule. You pay a set copay for each procedure regardless of how many treatments you need in a year.

- Dental discount plans: Not insurance, but membership programs that offer 15-40% off the provider's standard fees with no annual cap. These can be stacked with or used instead of insurance.

- Supplemental dental insurance: A second policy purchased individually to provide additional coverage above what your primary plan pays.

Annual Maximums and Inflation: A Shrinking Benefit

Perhaps the most frustrating aspect of dental insurance annual maximums is how little they have grown compared to the cost of dental care. When dental insurance first became widely available in the 1970s, the typical annual maximum was $1,000 to $1,500. Half a century later, the most common cap remains in that same range.

Meanwhile, the ADA reports that dental fees have increased an average of 4.2% per year over the past decade, with certain procedures seeing even sharper increases. A single porcelain crown that cost $600 in 2000 now costs $1,200-$1,600 in 2026. This means your annual maximum buys roughly half the dental care it did a generation ago.

What to Do When You Exceed Your Maximum

If you have already hit your annual maximum and still need treatment, you have several options:

- Defer non-urgent treatment to the next benefit year if your dentist confirms it is safe to wait.

- Use a Health Savings Account (HSA) or Flexible Spending Account (FSA) to cover the remaining costs with pre-tax dollars.

- Apply for third-party financing through providers like CareCredit, which offer 0% APR promotional periods of 6-24 months.

- Ask your dentist about an in-office payment plan that spreads the cost over several months without interest.

- Explore dental schools in your area, which offer supervised treatment at 50-70% of private-practice fees.

FAQ: Your Questions About Annual Maximums

In most plans, no -- unused benefits expire at the end of the benefit year. However, a growing number of carriers (including Delta Dental and Cigna) now offer rollover provisions on select plans, allowing $250-$500 of unused benefits to carry forward if you completed at least one preventive visit. Ask your employer or insurer whether your specific plan includes a rollover feature.

No. Your deductible is the amount you must pay out of pocket before insurance begins covering services. It is a separate threshold from the annual maximum. Only the amounts your insurer pays toward covered claims count against the annual maximum.

Most dental plans operate on a calendar-year basis (January 1 to December 31), meaning your annual maximum resets on January 1. However, some plans -- especially those purchased on the individual market or through certain employers -- use a "plan year" that may start on a different date, such as July 1 or the date you enrolled. Check your Summary of Benefits for your plan's specific benefit period.

It depends on your anticipated needs. If you only need preventive care, the lower-premium plan with a $1,500 maximum is usually the better value. But if you know you will need a crown, implant, or other major procedure, upgrading to a plan with a $3,000-$5,000 maximum can save you hundreds of dollars even after accounting for the higher premiums. Run the numbers for your specific situation before open enrollment closes.

Sources

- National Association of Dental Plans. "2026 Dental Benefits Report: Trends in Plan Design and Utilization."

- American Dental Association Health Policy Institute. "Dental Care Cost and Utilization Trends." March 2026.

- Delta Dental. "Understanding Your Annual Maximum and Rollover Benefits." 2026 Member Guide.

- Bureau of Labor Statistics. "Consumer Price Index: Dental Services." February 2026 Release.

- Journal of the American Dental Association. "Out-of-Pocket Dental Expenditures and Insurance Coverage Gaps in the United States." Vol. 157, No. 1, 2026.