Contents

Dental Insurance Orthodontic Coverage in 2026: Braces, Aligners & Maximizing Your Benefits

Orthodontic treatment remains one of the largest out-of-pocket dental expenses American families face. In 2026, the average cost of comprehensive braces sits between $5,500 and $8,000, while clear aligner therapy can run from $3,500 to over $8,500 depending on case complexity. Whether you are a parent planning ahead for a child's treatment or an adult considering aligners for the first time, understanding how dental insurance handles orthodontics is essential for making informed financial decisions.

Unlike routine cleanings and fillings, orthodontic coverage follows its own set of rules -- separate lifetime caps, unique waiting periods, age-based restrictions, and coinsurance structures that differ sharply from the rest of your dental plan. This guide breaks down every factor you need to evaluate before committing to a treatment plan in 2026.

How Orthodontic Insurance Works Differently in 2026

Standard dental benefits are designed around preventive and restorative care: cleanings, exams, X-rays, fillings, and crowns. Orthodontic benefits, by contrast, are classified as a specialty rider -- an add-on that many plans include but some do not. Even when a plan advertises "orthodontic coverage," the structure of that benefit is fundamentally different from other dental categories.

The most critical distinction is how the plan caps its payout. Regular dental benefits operate on an annual maximum -- a dollar limit that resets each calendar year (typically $1,000 to $2,500). Orthodontic benefits, however, are governed by a lifetime maximum that never resets. Once your plan pays its orthodontic cap, that benefit is gone permanently for that covered individual.

Key Insight for 2026

Starting with the 2026 plan year, several major carriers -- including Delta Dental Premier and Cigna Dental -- have raised their standard orthodontic lifetime maximums from $1,500 to $2,000 on employer-sponsored group plans. This reflects rising treatment costs and competitive pressure from newer carriers entering the orthodontic market.

Lifetime Maximums vs Annual Maximums Explained

The lifetime maximum is the single most important number in your orthodontic benefit. Unlike an annual maximum for general dental care that resets every January, the orthodontic lifetime cap is a one-time allocation. Once your insurer pays that amount toward braces or aligners, no further orthodontic benefits will be available under that plan -- even if you stay enrolled for decades.

| Feature | Annual Maximum (General Dental) | Lifetime Maximum (Orthodontics) |

|---|---|---|

| Reset Frequency | Resets every plan year | Never resets |

| Typical Range (2026) | $1,000 -- $2,500 | $1,500 -- $3,500 |

| Applies To | Cleanings, fillings, crowns, etc. | Braces, aligners, retainers |

| Coinsurance | 80--100% preventive, 50--80% basic/major | Typically 50% |

| Waiting Period | 0--6 months for basic/major | 12--24 months (individual plans) |

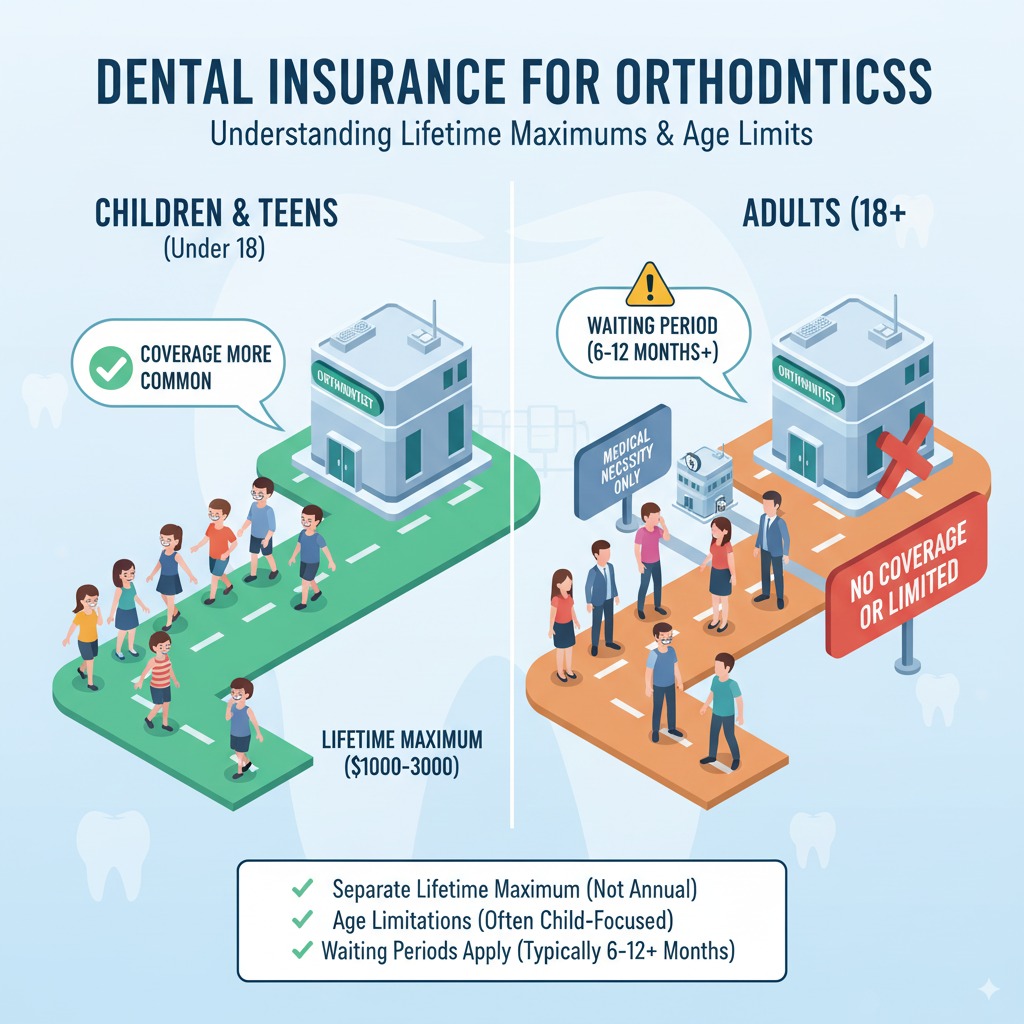

Age Limits and Adult Orthodontic Coverage Trends

Traditionally, orthodontic insurance was built around pediatric care. Most employer-sponsored plans still define orthodontic eligibility for dependents up to age 19 or, in some cases, age 26 when the dependent remains on a parent's medical plan under ACA provisions. However, the adult orthodontic market has expanded dramatically.

The American Association of Orthodontists reports that adults now account for roughly 30% of all orthodontic patients in the United States, up from just 20% a decade ago. Insurers have responded: as of 2026, approximately 65% of group dental plans that include orthodontic benefits now extend those benefits to adults with no age cap. Individual marketplace plans, however, remain more restrictive -- about 40% still limit orthodontic coverage to dependents under 19.

"The shift toward adult orthodontic coverage has been one of the most significant trends in dental insurance over the past five years. Employers now see it as a retention tool -- offering comprehensive orthodontic benefits helps attract and keep talent, especially among younger workers who prioritize smile aesthetics."

-- Dr. Rachel Nguyen, DDS, MS, Board-Certified Orthodontist and Insurance Policy Consultant

Important Warning

Even when a plan covers adult orthodontics, it may impose a lower lifetime maximum for adults compared to children. For example, some Aetna group plans offer a $2,000 lifetime max for dependents under 19 but only $1,000 for adults. Always read the plan summary carefully to confirm the specific benefit levels for your age group.

Covered Orthodontic Treatments: Braces, Aligners, and More

One of the most common questions patients ask is whether their insurance covers clear aligners like Invisalign or only traditional metal braces. The good news: in 2026, the overwhelming majority of dental plans with orthodontic benefits treat all FDA-approved orthodontic appliances equally. The benefit applies to the treatment, not the specific device.

Covered orthodontic treatments typically include:

- Traditional metal braces -- brackets and archwires bonded to teeth

- Ceramic (clear) braces -- tooth-colored brackets for a more discreet look

- Lingual braces -- brackets bonded behind the teeth

- Clear aligner therapy -- Invisalign, ClearCorrect, Spark, and other systems

- Diagnostic records -- panoramic X-rays, cephalometric films, digital scans, and photographs

- Retention appliances -- the first set of retainers at the end of active treatment

However, some treatments fall outside standard orthodontic coverage. Jaw surgery (orthognathic surgery) is typically classified as a medical procedure and must be billed through your medical insurance. Temporary anchorage devices (TADs) and some accelerated treatment modalities may or may not be included depending on your plan.

Comparing Orthodontic Coverage Across Major Insurers

Not all plans are created equal. The following comparison reflects standard 2026 offerings for employer-sponsored group plans. Individual plans may differ significantly.

| Carrier | Lifetime Max (Child) | Lifetime Max (Adult) | Coinsurance | Waiting Period (Group) |

|---|---|---|---|---|

| Delta Dental PPO | $2,000 | $2,000 | 50% | None |

| Cigna Dental | $2,000 | $1,500 | 50% | None |

| Aetna Dental | $2,000 | $1,000--$2,000 | 50% | None |

| MetLife PDP Plus | $2,500 | $2,500 | 50% | None |

| Guardian Dental | $1,500--$2,000 | $1,500 | 50% | None |

| Humana (Individual) | $1,000--$1,500 | Not covered | 50% | 12--24 months |

Understanding Coinsurance, Copays, and Cost Sharing

The industry standard for orthodontic coverage is 50% coinsurance. This means your insurer pays 50% of the approved fee and you pay the remaining 50%, up to the lifetime maximum. Some premium plans offer 60% or even 80% coinsurance, but these are uncommon and come with higher monthly premiums.

Here is how the math works in practice for a typical 2026 scenario:

Sample Cost Calculation

- Total treatment cost: $6,500

- Plan coinsurance: 50%

- Plan's share (50% of $6,500): $3,250

- Lifetime maximum: $2,000

- Insurance pays: $2,000 (capped at lifetime max)

- Your out-of-pocket cost: $4,500

The lifetime maximum functions as a hard ceiling. Even though the insurer's 50% share would be $3,250, the plan will only pay up to the $2,000 cap. This is why the lifetime maximum -- not the coinsurance percentage -- is the number that most affects your bottom line.

For DHMO (dental HMO) plans, the structure is different. Instead of coinsurance and a lifetime max, DHMO plans charge a fixed copayment for orthodontic treatment, often between $1,900 and $3,200 for comprehensive braces. This copay is the total patient responsibility, which can be lower than PPO out-of-pocket costs but requires using a designated in-network provider.

Orthodontic Waiting Periods: What to Expect

Waiting periods are one of the most frustrating aspects of orthodontic insurance, particularly for individual plans purchased outside of employer groups. These mandatory enrollment periods exist because insurers want to prevent people from buying a plan solely to get braces and then canceling once treatment begins.

Employer-sponsored group plans typically have no waiting period for orthodontic benefits. You are eligible from your plan's effective date. Individual and family plans purchased on the open market almost always impose a waiting period of 12 to 24 months for orthodontic services. A handful of carriers offer plans with no waiting period, but these tend to carry substantially higher premiums or lower lifetime maximums.

Planning Ahead

If you know orthodontic treatment is on the horizon, enroll in a plan with orthodontic benefits well before you plan to start. A 24-month waiting period means you need to be enrolled by early 2024 to access ortho benefits in 2026. Factor this timing into your financial planning.

Choosing the Right Plan for Orthodontic Benefits

When evaluating plans, focus on these five factors in order of financial impact:

- Lifetime maximum amount -- The single biggest driver of your savings. A plan with a $2,500 LTM saves you $1,000 more than one with $1,500.

- Waiting period length -- A 24-month wait effectively adds two years of premium payments before you receive any orthodontic benefit.

- Age restrictions -- Confirm whether adults are covered and at what benefit level.

- Network size -- A larger PPO network gives you more provider choices and negotiated rates.

- Monthly premium -- Compare the total cost of premiums over the waiting period plus treatment duration against the lifetime maximum benefit.

"I always tell my patients to do a simple break-even analysis. Add up all the premiums you will pay during the waiting period and the treatment period, then subtract the lifetime maximum you will receive. If you come out ahead by at least $500, the plan is worth it. If the math is close to even or negative, you may be better off negotiating a cash discount directly with the orthodontist."

-- Mark Sullivan, CFP, Healthcare Financial Advisor

Proven Strategies to Maximize Orthodontic Insurance

Getting the most from your orthodontic benefits requires proactive planning. Here are the most effective strategies for 2026:

- Request a pre-determination of benefits. Before starting treatment, have your orthodontist submit a treatment plan to your insurer. The insurer will issue a written estimate of what they will pay. This eliminates guesswork and prevents billing surprises.

- Use an in-network orthodontist. In-network providers have agreed to discounted fee schedules. Even before your lifetime max kicks in, you benefit from lower contracted rates. On a PPO plan, the in-network negotiated rate for comprehensive braces might be $5,200 versus a retail fee of $6,500 -- saving you $1,300 regardless of your insurance benefit.

- Coordinate benefits if both spouses have coverage. If you and your spouse each carry dental plans with orthodontic benefits, you may be able to coordinate benefits. The primary plan pays first up to its lifetime max, and the secondary plan may cover a portion of the remaining balance. This strategy can effectively double your insurance payout.

- Stack insurance with an FSA or HSA. Contribute pre-tax dollars to a Flexible Spending Account or Health Savings Account to cover your out-of-pocket share. At a 30% marginal tax rate, putting $4,000 into an FSA for orthodontics effectively saves you $1,200 in taxes.

- Time treatment start around the plan year. If your plan issues orthodontic payments on a quarterly or annual installment basis, starting treatment at the beginning of the plan year ensures you maximize the payment schedule.

Alternative Payment Options Beyond Insurance

Insurance alone rarely covers the full cost of orthodontic treatment. Fortunately, multiple financing options exist to bridge the gap:

- HSA and FSA accounts: Both can be used for orthodontic expenses. HSA funds roll over indefinitely, making them ideal for long-term treatment planning. FSA funds must be used within the plan year (with a possible $640 rollover in 2026).

- In-office payment plans: Most orthodontists offer zero-interest monthly payment plans spread over the duration of treatment (typically 18--24 months). Many practices require a down payment of $500--$1,000 with the remainder divided into equal monthly installments.

- Third-party financing: CareCredit, Lending Club, and Proceed Finance offer healthcare loans with promotional 0% interest periods ranging from 6 to 24 months. After the promotional period, interest rates typically jump to 17--27% APR, so plan to pay off the balance before the promotion ends.

- Dental discount plans: Not insurance, but membership programs (such as DentalPlans.com and Careington) that offer 20--30% discounts on orthodontic treatment at participating providers. Annual fees run $80--$200 per individual.

- Orthodontic school clinics: University dental schools and orthodontic residency programs offer treatment at 30--60% of private practice fees. Treatment is supervised by faculty and performed by residents in training. Wait times can be longer, but the savings are substantial.

Conclusion: Building Your Orthodontic Financial Plan

Orthodontic insurance in 2026 is more accessible and more generous than it has been at any point in the past decade. Lifetime maximums are rising, adult coverage is becoming standard on group plans, and clear aligners are treated equally with traditional braces by nearly every major insurer. However, the fundamental challenges remain: lifetime caps still cover only a fraction of treatment costs, waiting periods on individual plans can delay treatment by up to two years, and navigating the fine print requires diligence.

The most successful financial approach combines multiple strategies: securing the best available insurance benefit, pairing it with tax-advantaged accounts like an HSA or FSA, requesting a pre-determination before starting treatment, and negotiating an in-office payment plan for the remaining balance. By taking these steps before your first orthodontic appointment, you can reduce your total out-of-pocket cost by 40--60% compared to paying retail without any planning.

FAQ: Orthodontic Insurance Questions Answered

An annual maximum is the total amount your plan pays for general dental services (cleanings, fillings, crowns) within a single plan year, and it resets every year. An orthodontic lifetime maximum is a one-time benefit -- the total amount the plan will ever pay toward braces or aligner treatment for one individual. It never resets, even if you remain enrolled for many years.

In 2026, the vast majority of dental plans with orthodontic benefits do not differentiate between braces and clear aligners. The insurance benefit applies to the orthodontic treatment itself, not the specific appliance. However, a small number of older plans or discount-tier plans may exclude aligners or cap aligner benefits at a lower amount. Always confirm with your carrier before starting treatment.

Yes, if both you and your spouse have dental plans with orthodontic benefits, you can coordinate benefits. The primary plan pays first up to its lifetime maximum, and the secondary plan may then cover a portion of the remaining balance. The combined payout cannot exceed the total treatment cost. Contact both insurers to understand how coordination of benefits works under their specific policies.

This is known as a "treatment in progress" or "takeover" situation. Your new plan may offer a pro-rated benefit based on the remaining treatment time. For example, if you have 12 months of treatment left on a 24-month plan, the new insurer might cover 50% of the lifetime maximum. Some plans refuse to cover treatment already in progress. Coordinate with both carriers and your orthodontist's billing office before making the switch to avoid a coverage gap.

Yes, orthodontic treatment qualifies as a deductible medical expense on your federal income tax return. However, you can only deduct medical expenses that exceed 7.5% of your adjusted gross income (AGI). For most taxpayers, this threshold is difficult to reach unless you have significant medical expenses in the same tax year. Using an HSA or FSA is generally a more effective tax strategy for most families.

Sources

- American Association of Orthodontists, "Economics of Orthodontics Survey," 2025 Annual Report

- National Association of Dental Plans, "Dental Benefits Report: Trends in Enrollment and Plan Design," 2025

- Delta Dental Plans Association, "2026 Employer Group Plan Summary of Benefits," January 2026

- Cigna Healthcare, "Dental Plan Orthodontic Benefit Schedule," 2026 Plan Year

- U.S. Internal Revenue Service, "Publication 502: Medical and Dental Expenses," Tax Year 2025

- American Dental Association, Health Policy Institute, "Dental Insurance Coverage in the United States," 2025