Contents

PPO vs. HMO Dental Insurance in 2026: Costs, Networks & How to Choose the Right Plan

Roughly 164 million Americans carry some form of dental insurance, and for most of them, the plan they are enrolled in falls into one of two categories: a PPO (Preferred Provider Organization) or an HMO (Health Maintenance Organization, often called DHMO when applied to dentistry). These two plan structures represent fundamentally different approaches to balancing cost, access, and flexibility -- and choosing between them is one of the most consequential healthcare decisions you will make each enrollment period.

In 2026, the U.S. dental insurance market has surpassed $100 billion in total annual premiums, driven by rising awareness of the connection between oral health and systemic conditions like cardiovascular disease and diabetes. Whether you are selecting a plan through your employer, shopping on the individual marketplace, or evaluating options for your family, this guide will equip you with the knowledge to make a confident, financially sound choice.

The Fundamental Trade-Off: Cost vs. Flexibility

At its core, the PPO-versus-HMO decision comes down to a single question: Do you want lower monthly costs with restricted provider access, or higher monthly costs with the freedom to see any dentist?

PPO plans dominate the commercial dental insurance market, accounting for approximately 82% of all employer-sponsored dental plans in 2026 according to the National Association of Dental Plans. Their market dominance reflects a strong consumer preference for provider choice -- but that preference comes at a measurable cost. Understanding the mechanics of each plan type will help you determine which trade-off serves your situation best.

Quick Decision Framework

If you already have a dentist you trust and want the freedom to see specialists without referrals, a PPO is likely your better option. If you are primarily concerned with keeping monthly premiums low and your dental needs are mostly preventive, a DHMO may save you hundreds of dollars per year.

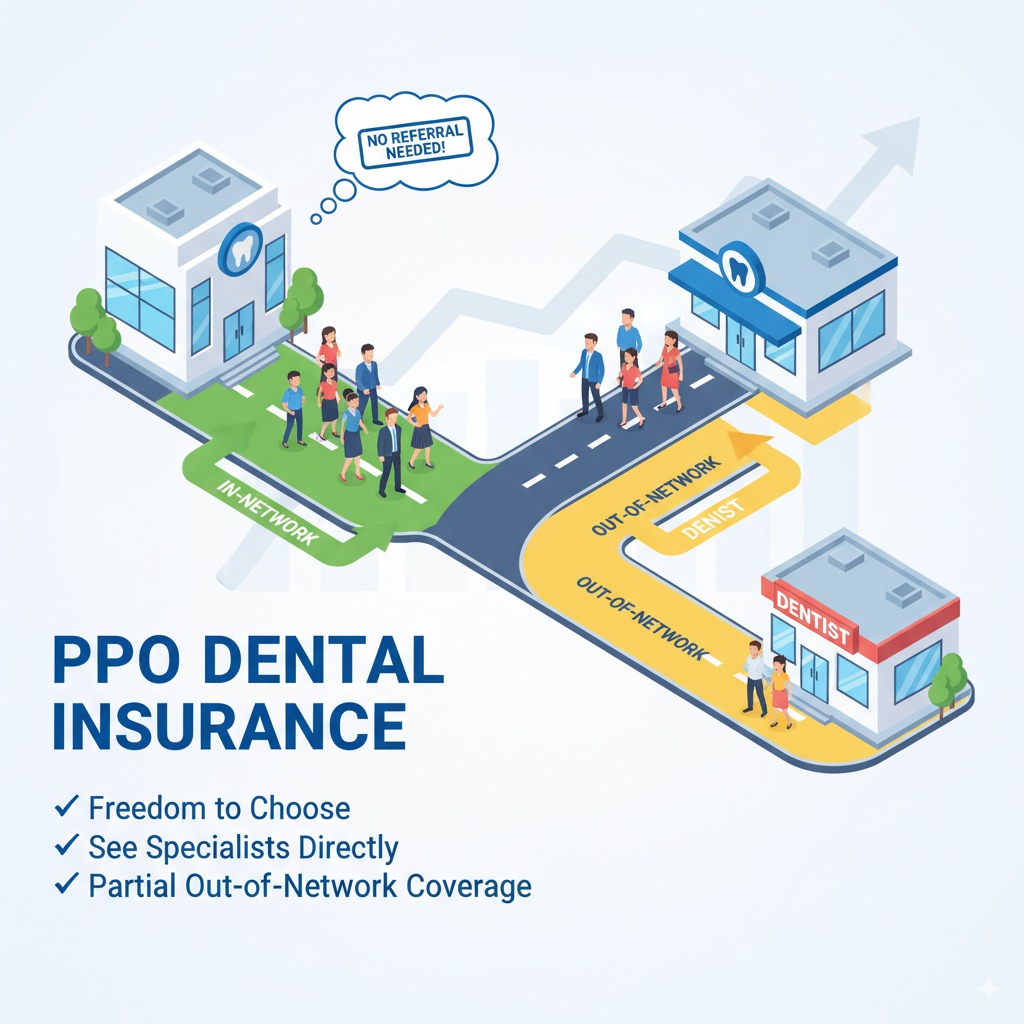

How Dental PPO Plans Work in 2026

A dental PPO operates through a contracted network of dentists who have agreed to accept discounted fees in exchange for patient volume. The plan pays a percentage of the dentist's fee based on a schedule that categorizes services into tiers: preventive, basic, and major.

The typical PPO benefit structure in 2026 looks like this:

- Preventive care (cleanings, exams, X-rays): Covered at 100% in-network with no deductible

- Basic procedures (fillings, simple extractions, root canals): Covered at 70--80% after deductible

- Major procedures (crowns, bridges, dentures, implants): Covered at 50% after deductible

- Annual deductible: Typically $50 per individual, $150 per family

- Annual maximum: $1,500 to $2,500 per person

The key advantage of a PPO is provider freedom. You can visit any licensed dentist -- in-network or out-of-network. When you stay in-network, you benefit from the insurer's pre-negotiated rates. When you go out-of-network, the plan still pays benefits, but you will owe more because the plan reimburses based on a "usual, customary, and reasonable" (UCR) fee schedule that is often lower than the out-of-network dentist's actual charges.

PPO Plan Advantages and Drawbacks

- Advantage: See any dentist without a referral, including specialists

- Advantage: Large nationwide networks -- Delta Dental alone has over 155,000 participating dentist locations

- Advantage: Out-of-network coverage still available (at reduced benefit levels)

- Advantage: No primary care dentist assignment required

- Drawback: Higher monthly premiums ($35--$65/month for individuals, $90--$170/month for families)

- Drawback: Annual deductibles must be met before basic and major services are covered

- Drawback: Annual maximums cap total plan payouts, which can be limiting for major work

"For patients who value continuity of care and already have an established relationship with a dentist, the PPO structure is hard to beat. The ability to see your existing provider without switching, and to access specialists directly when needed, has tangible health benefits beyond just convenience."

-- Dr. James Hartwell, DDS, Past President, Academy of General Dentistry

How Dental HMO (DHMO) Plans Work in 2026

A Dental HMO -- technically called a DHMO -- uses a managed-care model in which you select a primary care dentist (PCD) from a restricted network. All your care flows through this assigned dentist, who serves as a gatekeeper for specialist referrals. In exchange for accepting these limitations, you get significantly lower costs and more predictable out-of-pocket expenses.

The DHMO cost structure replaces the percentage-based coinsurance model used by PPOs with a fixed copayment schedule. Rather than paying 20% or 50% of a procedure's cost, you pay a flat dollar amount listed on the plan's fee schedule. Common 2026 DHMO copayments include:

- Preventive exam and cleaning: $0--$10

- Composite filling (one surface): $25--$45

- Root canal (anterior tooth): $125--$250

- Porcelain crown: $250--$450

- Simple extraction: $15--$35

DHMO Plan Advantages and Drawbacks

- Advantage: Very low monthly premiums ($8--$25/month for individuals, $25--$60/month for families)

- Advantage: No annual deductibles on most plans

- Advantage: No annual maximum -- your benefits are not capped

- Advantage: Predictable copayments make budgeting straightforward

- Drawback: Must use in-network providers only -- zero coverage for out-of-network care

- Drawback: Must select and use a primary care dentist

- Drawback: Specialist visits require a referral from your PCD

- Drawback: Networks are smaller and geographically limited

Geographic Availability Warning

DHMO plans are not available in every state. As of 2026, DHMO plans are most commonly offered in California, Texas, Florida, Arizona, and Nevada. If you live in a rural area or a state with limited DHMO networks, a PPO plan may be your only practical option. Always verify network availability in your specific ZIP code before enrolling.

Side-by-Side Comparison: PPO vs. HMO

| Feature | Dental PPO | Dental HMO (DHMO) |

|---|---|---|

| Monthly Premium (Individual) | $35--$65 | $8--$25 |

| Monthly Premium (Family) | $90--$170 | $25--$60 |

| Annual Deductible | $50 individual / $150 family | None |

| Annual Maximum | $1,500--$2,500 | None |

| Provider Choice | Any dentist (in or out-of-network) | In-network only |

| Specialist Access | Direct, no referral needed | Requires PCD referral |

| Cost Structure | Percentage-based coinsurance | Fixed copayments |

| Claim Filing | Provider files; out-of-network may require patient filing | Provider handles all billing |

| Nationwide Coverage | Yes | Limited to service area |

| Best For | Those wanting flexibility and choice | Budget-conscious individuals and families |

Real Cost Scenarios: PPO vs. HMO

Abstract comparisons only go so far. Let us examine what each plan type costs in three real-world scenarios using 2026 pricing.

| Scenario | PPO Total Annual Cost | DHMO Total Annual Cost | Savings With |

|---|---|---|---|

| Preventive Only (2 cleanings, 1 exam, bitewing X-rays) | $540 (premiums only; care at 100%) | $192 (premiums + $0 copays) | DHMO saves $348 |

| Moderate Use (preventive + 2 fillings + 1 root canal) | $540 premiums + $50 deductible + $210 coinsurance = $800 | $192 premiums + $70 fillings + $175 root canal = $437 | DHMO saves $363 |

| Heavy Use (preventive + crown + implant + 3 fillings) | $540 premiums + $50 deductible + $1,800 coinsurance = $2,390 (may hit annual max) | $192 premiums + $400 crown + $950 implant + $105 fillings = $1,647 | DHMO saves $743 |

The Annual Maximum Factor

In the heavy-use scenario, the PPO's $2,000 annual maximum becomes a critical limitation. Once the plan has paid its $2,000, you are responsible for 100% of any additional treatment costs for the rest of the year. The DHMO has no annual cap, so your copay schedule remains in effect regardless of how many procedures you need. This makes DHMOs particularly advantageous for patients anticipating significant dental work.

Market Trends Shaping Dental Insurance in 2026

Several developments are reshaping the dental insurance landscape and affecting the PPO-versus-DHMO decision:

- Teledentistry integration. Both PPO and DHMO plans now routinely include virtual consultations for initial assessments, post-procedure follow-ups, and oral health coaching. Teledentistry visits carry $0 copays on most plans, reducing unnecessary in-office visits.

- Preventive-first plan designs. Insurers are increasingly covering fluoride treatments, sealants, and periodontal screenings at 100% even for adults, recognizing that every dollar spent on prevention saves $8--$50 in restorative care downstream.

- Implant coverage expansion. Dental implants were historically excluded from most plans. In 2026, an estimated 45% of PPO plans and 30% of DHMO plans now include implant benefits, though coverage levels and copays vary widely.

- Hybrid plan emergence. A small but growing category of plans blends PPO and HMO features -- offering HMO-style copays for in-network providers and limited PPO-style out-of-network benefits. Carriers like Anthem and UnitedHealthcare are piloting these designs in select markets.

- ACA pediatric dental requirements. Under the Affordable Care Act, dental coverage for children remains an essential health benefit. Marketplace plans must include pediatric dental benefits, and many states have expanded the definition of covered services for children under 19.

"We are seeing a convergence in plan design that was unthinkable ten years ago. The rigid boundaries between PPO and HMO are softening as carriers experiment with hybrid models. Consumers benefit because competition forces every plan type to offer more value -- whether through broader networks, richer benefits, or lower premiums."

-- Karen Phillips, Senior Analyst, National Association of Dental Plans

Which Plan Is Right for You?

Your ideal plan depends on several personal factors. Consider each of the following carefully:

Choose a PPO if:

- You have an established dentist you want to keep seeing, regardless of network status

- You travel frequently or live in a rural area with limited DHMO networks

- You anticipate needing specialist care and want direct access without referrals

- Your employer subsidizes the premium difference, making the out-of-pocket cost similar

- You prefer the flexibility to get a second opinion from a different provider

Choose a DHMO if:

- Keeping monthly premiums as low as possible is your top priority

- You live in a metro area with strong DHMO network coverage

- You are comfortable selecting a primary care dentist from a directory

- You need extensive dental work and want to avoid annual maximum limitations

- You prefer predictable, fixed copays over percentage-based coinsurance

Do the Math Before You Enroll

Calculate your total expected annual cost under each plan: 12 months of premiums + estimated deductibles + estimated copays or coinsurance for the procedures you anticipate needing. This total-cost comparison is far more meaningful than looking at the monthly premium alone. A plan with a $15/month premium that charges $400 for a crown may cost you more in total than a $50/month plan that covers that same crown at 50% after a $50 deductible.

Conclusion: Making a Strategic Plan Decision

The PPO-versus-DHMO decision is not a question of which plan type is objectively "better" -- it is about which one aligns with your specific circumstances. PPO plans offer unmatched flexibility and provider choice, making them the right fit for people who value autonomy in their healthcare decisions and can afford the higher premiums. DHMO plans deliver genuine cost savings and predictability, particularly for families and individuals who need substantial dental work and are comfortable operating within a structured network.

In 2026, both plan types are stronger than they have ever been. PPO networks continue to expand, annual maximums are gradually rising, and preventive coverage is nearly universal at 100%. DHMO plans are offering richer copay schedules, adding implant coverage, and integrating teledentistry options that make managed care more patient-friendly than before. Whichever path you choose, the most important step is to analyze your anticipated dental needs, run the numbers for both options, and make a data-driven decision during your next enrollment period.

FAQ: PPO vs. HMO Dental Insurance

In most cases, you can only change your dental plan during your employer's annual open enrollment period or within 30 days of a qualifying life event (such as marriage, birth of a child, or loss of other coverage). If you purchase an individual plan on the marketplace, open enrollment typically runs from November through mid-January for coverage starting the following year.

Yes. One of the major advantages of PPO plans is their nationwide network coverage. Most PPO carriers maintain networks across all 50 states. Even if the dentist you visit in another state is out-of-network, your PPO plan will still provide out-of-network benefits -- though at a lower reimbursement rate. DHMO plans, by contrast, are generally restricted to a specific geographic service area and provide zero coverage outside that zone.

Increasingly, yes. About 30% of DHMO plans in 2026 include implant benefits with copays typically ranging from $800 to $1,500 per implant. This is still significantly less than the retail cost of $3,000 to $5,000 per implant. However, many DHMO plans still exclude implants entirely, so check your specific plan's fee schedule before assuming coverage.

Yes. Dental indemnity plans (also called fee-for-service plans) allow you to visit any dentist with no network restrictions. The plan reimburses a set percentage of the dentist's fee with no negotiated discounts. Indemnity plans offer the most freedom but come with the highest premiums and are relatively rare in the employer market. Additionally, dental discount plans (not insurance) offer reduced fees at participating providers for an annual membership fee, typically $80--$200 per year.

Your insurer will notify you and assign you a new primary care dentist from the network. You typically have the option to choose a different in-network provider instead. If you have treatment in progress, most plans allow a transition period to complete active procedures with a temporary provider. Contact your insurer's member services as soon as you receive notice of the change.

Sources

- National Association of Dental Plans, "2025-2026 Dental Benefits Report: Enrollment Trends and Plan Design," 2025

- American Dental Association, Health Policy Institute, "Dental Insurance Coverage and Utilization in the United States," 2025

- Delta Dental Plans Association, "Network Size and Provider Participation Report," January 2026

- Centers for Medicare and Medicaid Services, "Marketplace Dental Plan Enrollment Data," 2026 Plan Year

- Bureau of Labor Statistics, "Employee Benefits in the United States -- Dental Plan Access and Take-Up Rates," March 2025

- Kaiser Family Foundation, "Employer Health Benefits Survey -- Dental Benefits Section," 2025